The following are general principles to consider in relation to calculating the amount of financial provision required.

The scope of the exercise should be clear and be informed by law and guidance.

For unforeseen liabilities, for example under the Environmental Liability Directive, it should be clear whether complementary and/or compensatory remediation, as well as primary remediation, is covered. A risk assessment should then be undertaken to allow the determination of the maximum estimated liability.

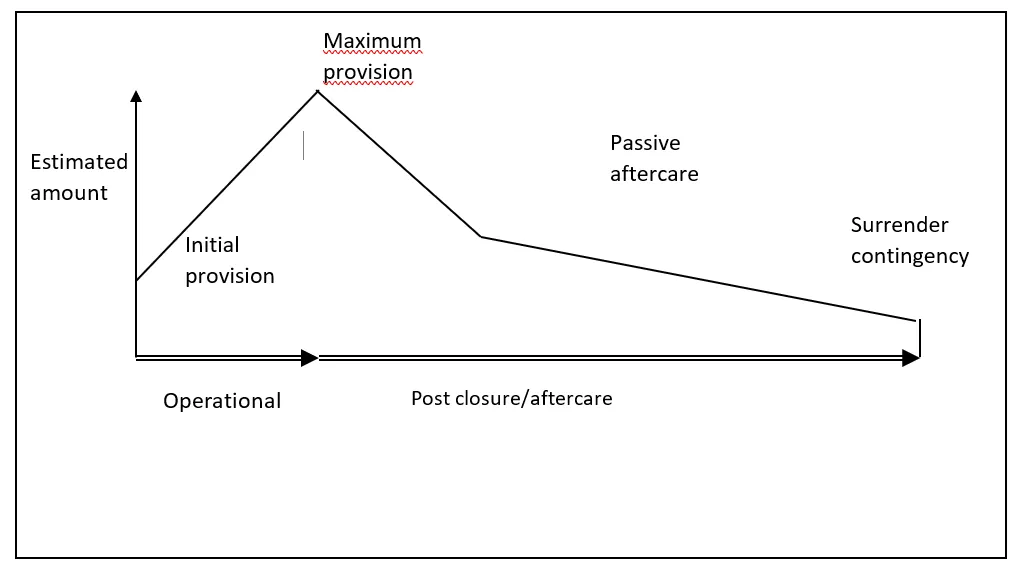

For foreseen liabilities, it is important to establish whether the liability remains the same throughout the life of the operation (for example, a waste treatment centre) or whether the liability is going to change throughout the life of the operation (for example, a landfill or a mine). In the case of mines and landfills the closure, restoration and aftercare costs extend over long periods and change over time. Key points throughout the duration of the operation (e.g. initial liability, maximum liability) and the ultimate end date should be established. This pattern of costs can be referred to as the ‘cost profile’ (see the figure below).